The FinOperator's view of FinOps

Wherein we discuss what an income statement is and why you should care about it, especially if you're not in the Finance team.

Housekeeping

Hello readers. I am two weeks into a new job, the first time I've said that since 2016. This post will be heavy on the prose, as I have left all my data and charting capability with which to illustrate my points behind. One of my first jobs in this new role is to rebuild my powers and thus build my employers capabilities in this area. Stay tuned.

Additionally, I made the decision sometime earlier this year that the focus of my writing here would be for the technical FinOps practitioner, engineer, or data person. This is my background, and so my vocabulary and background has the greatest overlap with technical staff, not Finance staff. I will be explaining basic finance concepts in this blog that will not be useful for the finance professional, and assuming technical background that the typical finance professional shouldn't be expected to have.

With that out of the way, I present to you:

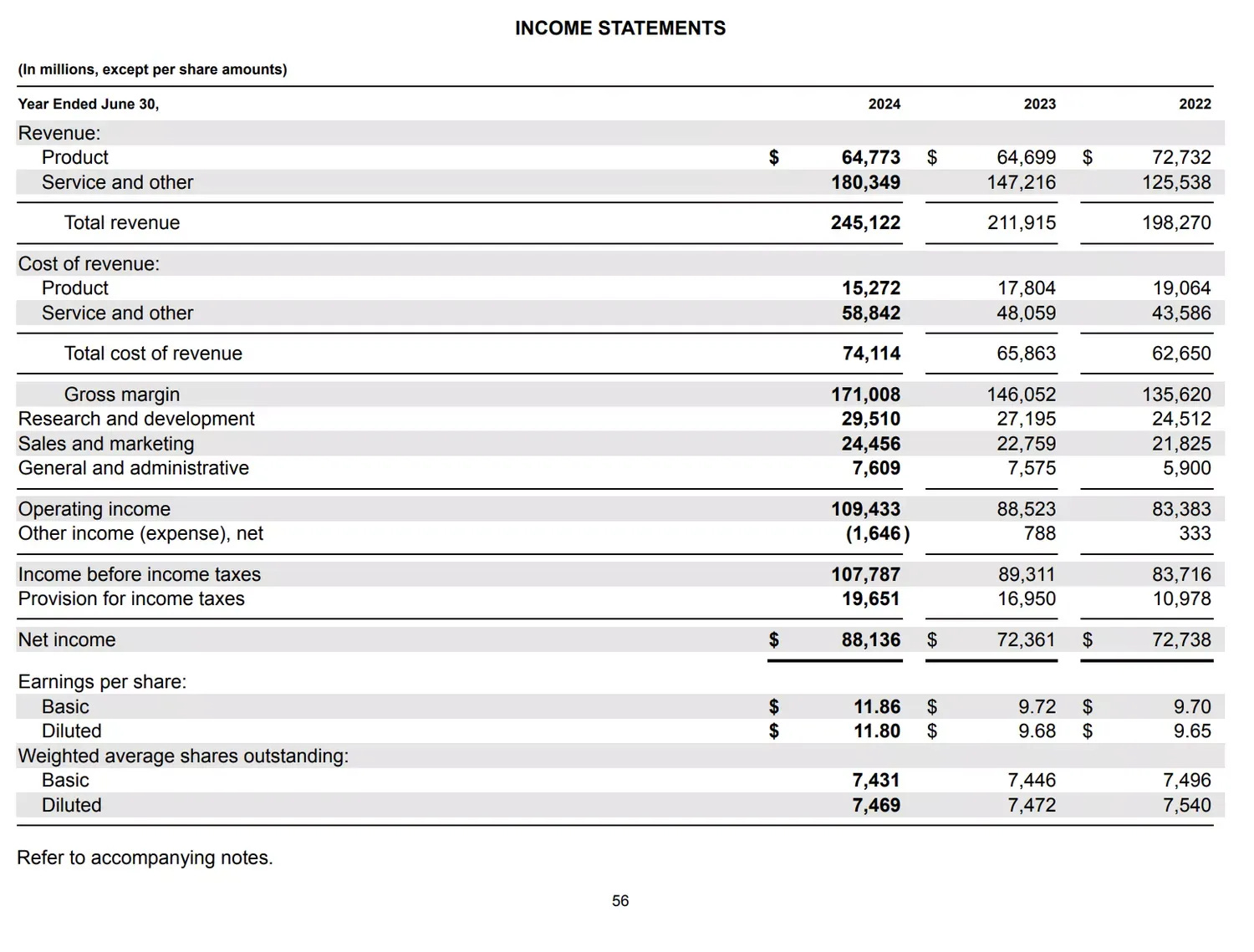

The Income Statement

Being new in a job, it’s a habit of mine to explain my point of view to my new teammates, so that they hopefully understand where I'm coming from someday. Early on my first week I explained to the overall team (I have 3 teams right now) that my mental framework for where to focus our efforts is often informed by thinking about the company's income statement. I didn't go into much detail on that.

Later, I was having a 1:1 with a member of the data team this week, an "AE" in the parlance of our times. We have a couple headcount open that we'll soon begin hiring for and I was voicing my wish to have one of the analyst hires to be focused on FinOps. Somewhere in there I said "COGS" and she said "wait, what?". We got into the structure of how the income statement works and because technical staff are often interviewed on SQL optimization techniques or how to invert a binary tree on a whiteboard, she hadn't been properly introduced to the income statement before.

Today we're going to take it high level and talk about an important topic that informs my conceptual framework for how I do FinOps. The Income Statement.

The topline

I picture the income statement as a funnel diagram. A Sankey will often be used as well, but I think the funnel maps very cleanly to the concepts from top to bottom. At the top of the statement you have your income, also known as revenue also known colloquially as, you guessed it, the "topline".

Because I work in the internet business, most of our industry's topline comes from sales of whatever our product is, or possibly professional services income from support it. If your company has investments in the form of $whatever (cash) earning interest then that'd also go in the topline section, but most of any company's revenue is going to come from selling the $thing that the company exists to sell.

Regardless of where it comes from, this is the money in at the top of the funnel. After/below this, the income statement is mostly an exercise in subtracting various categories of expenses before landing on the "bottom line".

💡 By the way, a very important point: you'll hear people say "P&L" as you work deeper into the business. Income statement == P&L. It's the same thing.

COGS, aka "cost of revenue", aka "cost of sales"

COGS is Cost of Goods Sold and I think of COGS as the sphere of my influence as a FinOps person. COGS is what it says - it's the cost of the things that are required to produce the goods or services that the company sells. You could put aside the funnel metaphor for a moment and think of COGS as the cost of the inputs required to produce the outputs that represent whatever your company sells to its customers.

In the last century this could be the cost of mining and shipping iron ore, and refining that ore into the steel that is ultimately sold for revenue. The next company in line would have the cost of the steel as part of their COGS to building the car that brings in their revenue. In the 21st century a typical company hosting products on a public cloud vendor like GCP or AWS would have (parts of) their cloud bills as the cost inputs to provide the service that nets the resulting revenue output. I'll come back to the "parts of" part later.

Other common COGS inputs are things like your support or professional services staff. Without them handling customers you don't have a sustainable business model, and so if the cost is in any way related to the function of the thing that is sold for revenue at your business, then it fairly belongs in COGS.

Below COGS - gross margin, operating costs, etc

Pull together your COGS, then subtract them from the topline and you arrive at an important metrics called gross margin. Below gross margin you subtract your operating costs - things like R&D, Marketing, Sales, and others - to arrive at your operating margin. R&D and Marketing might seem simple enough, but you'll definitely have things in your cloud bills that belong in these two categories, so you can't just dump the entire cloud bill into COGS and call it a day. "But it all lands at the bottom either way. Why does it matter whether it comes out in this section or that section?" A fabulous question that lives near the borders of my understanding of VC backed company finance.

In a nutshell, because it matters. The various major sections of your income statement are in place because they each tend to have a different relationship with scaling as revenue scales. If you are a cloud-based software provider, it is expected that parts of your operation will scale more efficiently than others as the overall business scales. IOW - as revenue grows your COGS will grow as well, but it will grow with a different slope than say, Marketing or R&D.

The average slope of these various segments within an average company in a given vertical is probably fairly well known by investor analysts, and so they will be able to model out your potential profitability if your income statement is tidy enough. They will be able to model, for example, if you have a 70% gross margin today what optimizations might take place over the next 5 years to land you at a 76% margin with 250MM ARR. These are all metrics and models they use to gauge your company's potential return on their investment.

On the other hand if you have a 65% gross margin today, how does that scale out to result in a vastly less profitable company (that they might pass on investing in)?

So, back to COGS

This is why it's so tremendously important to get the math right, and make sure that what is being allocated to COGS and what is being allocated elsewhere (we'll cover "Opex" eventually) is correct. This will be an extended conversation with your Finance team, because this analysis will require a thorough, transparent, and repeatable process of working with your cloud bills to improve tagging and visibility of the costs within them. This is why proper tagging matters in the first place. It's not just for improving the visibility of these costs, it plays a central role in proper cost allocation all the way down the line.

Zooming back out

The point of going through this is that the income statement can give you a lot of information about your company. Likely you'll need to make good friends with someone in Finance before they let you see it - it's privileged information - but I think it can tell you what to focus on as a data or FinOps person. In data broadly as well as FinOps specifically we are tasked with helping our employer better understand itself, and the income statement provides a framework for what strengths the company has that must be protected as well as its weaknesses that must be further developed. It's a very important map, without which you're missing critical information about the company you're trying to help.

However, even just thinking in this manner puts you ahead of most staff in most companies outside of Finance. After all, finance is a support function, engineering is a major driver of company outcomes.

In closing - understand the business you're in.